Why AI in Collections is a Strategic Imperative

Before diving into how to deploy AI in collections, let’s examine why timing matters. The business case for AI voice agents isn’t just compelling – it’s becoming essential for competitive survival.

The Cost-to-Collect Challenge

Collection operations are drowning in high-volume, repetitive tasks. Initial outreach calls, payment reminders, and simple account enquiries consume enormous human resources while delivering limited returns. AI can reduce these operational expenses by up to 40%, according to McKinsey analysis, by automating routine communications at a fraction of human labour costs.

Consider the maths: if your current cost per successful resolution is £25 using human agents, AI could potentially reduce this to £15 or lower for suitable use cases. Across thousands of accounts, these savings compound rapidly.

Scaling Beyond Human Limitations

Traditional collections face an inherent scalability ceiling. Want to contact more customers? Hire more agents. Need 24/7 coverage? Pay premium shift rates. AI voice agents shatter these constraints.

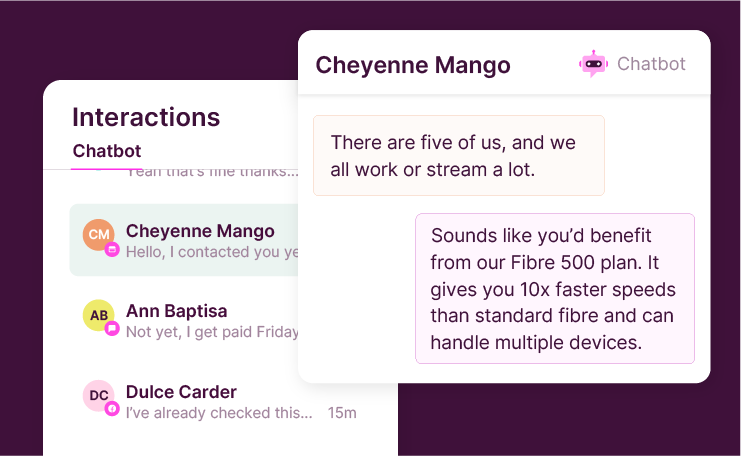

A single AI agent can handle hundreds of simultaneous calls, operate continuously, and achieve 100% account penetration – physically impossible with human teams. Case studies show remarkable results: 95% AI containment rates and 50%-80% payment plan acceptance rates when AI is deployed strategically.

The AI Analytics Advantage

Modern AI doesn’t just automate – it optimises. By analysing payment patterns, communication history, and demographic data, AI systems can predict the optimal time, channel, and approach for each individual debtor. This data-driven personalisation moves beyond generic strategies to tailored engagement that increases response rates significantly.

The Phased Deployment Playbook for AI Agents: Your Strategic Roadmap

The key to successful AI deployment in collections isn’t choosing between AI and humans-it’s creating a sophisticated blend that leverages each for what they do best.

Here’s your three-phase roadmap for getting it right.

Phase 1: Low-Risk Foundation (Months 1-6)

Objective: Prove ROI and build operational confidence with minimal risk exposure.

Target Use Cases:

- Payment reminders for early-stage delinquency (1-30 days)

- Promise-to-Pay confirmations

- Simple inbound enquiries (balance enquiries, payment dates)

- Self-service payment portal guidance

Why Start Here: These interactions are transactional, not persuasive. They leverage AI’s core strengths—consistency, availability, and scale—while minimising the risk of relationship damage. An ineffective reminder call might be ignored, but it won’t permanently harm your ability to collect.

Key Integrations Needed:

- CRM system for personalised data access

- Telephony platform or contact centre software

- Payment portal for seamless transactions

- Basic escalation workflows to human agents

Success Metrics:

- Containment rate (percentage resolved without human intervention)

- Cost per successful resolution

- Customer satisfaction scores for AI interactions

- Promise-to-Pay conversion rates

Phase 1 Checklist:

- Establish AI governance committee

- Select 1-2 vendors for pilot comparison

- Design A/B testing framework

- Complete technical integrations

- Train staff on AI oversight responsibilities

- Implement new KPI dashboard

Phase 2: Strategic Expansion (Months 6-18)

Objective: Scale proven use cases and pilot medium-complexity applications.

New Use Cases:

- Scripted payment plan offers within defined parameters

- Omnichannel outreach campaign management

- Basic dispute acknowledgment and routing

Enhanced Capabilities:

- More sophisticated decision-making based on customer data

- Dynamic payment plan generation within business rules

- Multi-channel coordination (voice, SMS, email)

- Advanced sentiment analysis for escalation triggers

Risk Management: Phase 2 introduces more autonomous decision-making, requiring robust governance. The AI begins offering solutions, not just communicating information. Monitor algorithmic bias carefully and ensure human oversight of all payment plans offered.

Training Evolution: Your human agents begin their transformation into specialists. Focus training on complex negotiation skills, vulnerability identification, and AI performance monitoring.

Phase 3: Mature Blended Operations (Months 18+)

Objective: Operate a fully optimised AI-human hybrid model.

AI Responsibilities:

- All high-volume, transactional communications

- Early-stage recovery for suitable accounts

- 24/7 inbound support for routine enquiries

Human Agent Focus:

- Complex negotiations and settlements

- Vulnerable customer interactions

- Dispute resolution and complaints

- High-value account management

- AI system oversight and optimisation

The New Agent Role: Your collection agents evolve into highly skilled specialists. Some become “Human Interaction Specialists” focussed on empathy and complex problem-solving. Others become “AI Performance Analysts” who monitor, coach, and optimise the automated systems.

Overcoming the Persuasion Gap: The Critical Success Factor

Here’s what many AI vendors won’t tell you: AI significantly underperforms humans in persuasive conversations. Academic research from leading universities reveals a critical “persuasion gap” – promises made to AI agents are less likely to be kept and even brief AI contact, if not done right, can permanently impair long-term recovery rates.

It’s a fundamental challenge that determines whether your AI deployment succeeds or fails.

The Research Reality

A controlled study at a major financial services firm found that accounts initially contacted by AI showed persistently lower recovery rates over a full year, even after human agents took over. The moral weight of a promise made to a machine simply isn’t equivalent to one made to a person.

The Strategic Response

This research doesn’t invalidate AI – it clarifies its optimal role. Use this decision matrix for call routing:

Compliance and Governance Essentials

Deploying AI in collections isn’t just a technology decision-it’s a regulatory responsibility. The FCA’s Consumer Duty, GDPR, and other frameworks create a complex compliance landscape that must be navigated carefully.

FCA Consumer Duty Requirements

The Consumer Duty demands good outcomes for customers. Your AI systems must demonstrably deliver fair treatment across all customer segments. Key requirements include:

- Bias Detection: Regular auditing to ensure AI doesn’t discriminate against protected groups

- Vulnerability Identification: Automatic escalation when AI detects customer distress or hardship indicators

- Outcome Monitoring: Continuous measurement of customer outcomes, not just operational efficiency

GDPR and Data Protection

AI processing involves personal data at every step. Ensure compliance through:

- Transparent Communication: Customers must know they’re speaking with AI from the conversation start

- Lawful Basis: Establish clear legal grounds for processing (typically legitimate interests in collections)

- Data Subject Rights: Build systems that facilitate access requests and data erasure

Governance Framework Essentials

Create a cross-functional AI Ethics and Governance Committee with representatives from Risk, Compliance, Legal, IT, and Operations. This body should:

- Approve new AI use cases

- Review performance against fairness metrics

- Investigate edge cases and complaints

- Maintain the authority to override or disable AI systems

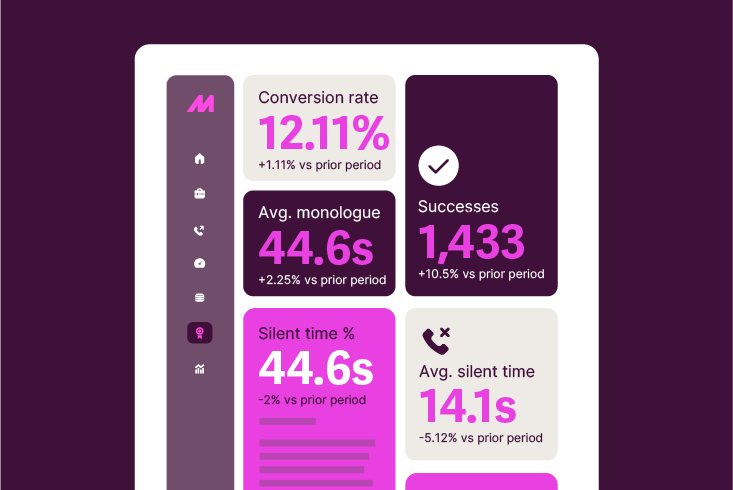

Measuring ROI Beyond Cost Savings

Traditional ROI calculations often miss the full picture. Here’s a comprehensive framework for measuring AI impact in collections:

Efficiency Metrics

- Cost per contact reduction

- Agent productivity improvement

- Processing time reduction

- 24/7 availability value

Effectiveness Metrics

- Promise-to-Pay conversion rates (AI vs. human)

- Promise fulfilment rates (the critical measure)

- Long-term recovery rate impact

- Customer satisfaction scores

Quality Metrics

- Compliance breach reduction

- Audit trail completeness

- Escalation appropriateness

- Customer complaint rates

The A/B Testing Imperative

Don’t rely on vendor claims. Implement rigorous A/B testing with statistically significant sample sizes. Track not just immediate outcomes but long-term repayment behaviour over 6-12 months. This data-driven approach provides the objective evidence needed for informed scaling decisions.

Common Deployment Pitfalls and How to Avoid Them

Pitfall 1: Over-Reliance on Vendor Promises

Solution: Demand proof-of-concept pilots with your actual data and customer base before committing to large-scale deployment.

Pitfall 2: Deploying AI in High-Risk Scenarios Too Soon

Solution: Stick to the phased approach. Resist pressure to accelerate into complex use cases before proving fundamentals.

Pitfall 3: Neglecting Change Management

Solution: Invest heavily in reskilling your workforce. The human element remains crucial for AI success.

Pitfall 4: Inadequate Governance Structure

Solution: Establish formal oversight before deployment, not after problems arise.

Pitfall 5: Ignoring the Persuasion Gap

Solution: Design your system around AI’s limitations, not just its strengths.

Your Quick-Start Implementation Checklist

Before You Begin

- Audit current technology stack compatibility

- Assess internal development capabilities

- Define success metrics and KPIs

- Establish governance committee

- Secure senior leadership sponsorship

Vendor Selection

- Prioritise collections-specific experience

- Verify compliance certifications (PCI-DSS, SOC 2)

- Test conversational quality with real scenarios

- Evaluate integration complexity

- Understand total cost of ownership

Pilot Preparation

- Select low-risk use case portfolio

- Design A/B testing methodology

- Complete technical integrations

- Train oversight team

- Establish escalation protocols

Go-Live Support

- Monitor performance metrics daily

- Review AI interactions for quality

- Gather customer feedback

- Document lessons learned

- Plan Phase 2 expansion

The Path Forward: Maximising Every Moment

AI voice agents represent a transformational opportunity for debt collection operations, but success demands a nuanced, strategic approach. The organisations that thrive will be those that deploy AI thoughtfully, respect its limitations, and create sophisticated hybrid models that amplify human capabilities rather than simply replacing them.

The question isn’t whether to deploy AI in collections – it’s how to do it right. By following this phased playbook, you can harness AI’s power to reduce costs, scale operations, and improve customer experiences while preserving the human relationships that drive long-term recovery success.

Remember: you’re not just implementing technology. You’re reimagining how collections work in an AI age. Get it right, and you’ll create a sustainable competitive advantage that maximises every moment of customer interaction.

Ready to see how AI agents can transform your collections operation? Let’s talk about your specific challenges and explore how MaxContact’s digital voice agents can help you recover more debt while keeping overheads controlled.

References

- The Promise of Generative AI for Credit Customer Assistance – McKinsey

- Better than Human? Experiments with AI Debt Collectors – University of Alberta

- NBER Working Paper – How Good is AI at Twisting Arms? – Choi, Huang, Yang

- AI Regulation in Financial Services: FCA Developments – Regulation Tomorrow