The FCA has moved from implementation to active enforcement, with four cross-cutting supervisory reviews now underway and the next annual board report due by 31 July 2026. The question regulators are asking is no longer "have you implemented Consumer Duty?" It's "can you demonstrate, with evidence, that your firm is delivering consistently good outcomes for retail customers?"

For contact centre teams, that shift matters enormously. The contact centre is where Consumer Duty either gets evidenced or falls apart. Call scripts, agent behaviour, handling of vulnerable customers, complaint resolution and call quality data are all in scope. If you can't produce the evidence, the regulator will assume you don't have it.

This guide covers what the Duty requires, what changed in 2025 and 2026, and what your contact centre needs to do to stay on the right side of it. It covers debt collection, insurance, banking and credit; anywhere your contact centre serves retail customers under FCA regulation.

What changed in 2025 and 2026

The FCA has shifted from supervision to scrutiny. The regulator reviewed board reports from 180 firms and published detailed good and poor practice guidance. The consistent finding: firms are producing compliance documents without producing compliance evidence. The FCA wants data, MI and documented outcomes, not assertions.

The FCA’s four focus areas for 2026 include: how firms design products and services to meet customer needs; how firms monitor consumer outcomes; how firms design customer journeys (with specific scrutiny of friction); and whether firms' communications help customers make informed decisions. Contact centres sit in the middle of three of those four.

Enforcement consequences now apply. For serious or persistent failures, the FCA can issue public censure, financial penalties and, where SM&CR applies, individual accountability action against named senior managers. This is no longer a paper exercise with soft consequences.

Debt collection is under specific scrutiny in 2026. Collections contact strategies covering call frequency, agent conduct, handling of payment difficulty and identification of vulnerable customers are directly in the FCA's sights under Consumer Duty's "avoid foreseeable harm" rule. Firms in collections must evidence that their contact strategies are not causing consumer harm.

The July 2026 board report deadline is approaching. Every FCA-regulated firm must have its annual Consumer Duty board report reviewed and approved by its governing body by 31 July 2026. The report needs to demonstrate outcomes monitoring data, identify any customer groups receiving worse outcomes and set out remediation plans. If your contact centre doesn't have that data, your board report won't hold up.

The four outcomes and what they mean for your contact centre

Products and services

The products and services outcome requires firms to ensure that what they're selling, collecting on or supporting is genuinely designed to meet the needs of the customers being served.

For contact centres, the practical question is: are your agents accurately representing what a product does and doesn't do? Are call scripts designed to help customers understand, or to move them through a process quickly? Are there different approaches for different customer segments, including those in financial difficulty or with characteristics of vulnerability?

In debt collection specifically, this outcome applies to the repayment arrangements being offered. If your collections contact strategy is pushing customers toward arrangements that aren't suitable for their circumstances, that's a Consumer Duty exposure.

Price and value

Customers must receive fair value; a reasonable relationship between cost and benefit. For contact centres, this outcome is most relevant where agents are selling, upselling or explaining pricing.

The FCA expects firms to evidence that they've assessed fair value and acted on the results. If your QA monitoring is revealing agents mis-explaining charges, or customers repeatedly calling back because they didn't understand what they signed up for, that's both a consumer support failure and a price and value signal.

For insurance contact centres, this is an area of active FCA scrutiny. The regulator's pure protection insurance market study is examining whether customers in that sector are receiving fair value, and contact centre conduct data is part of what firms will need to produce.

Consumer understanding

Customers must receive communications they can understand, at the right time and in a format that supports informed decision-making. For contact centres this is the most direct outcome; every call is a test of it.

The FCA's cross-cutting review on customer communications is examining whether information helps customers make genuinely informed decisions, or nudges them toward commercially convenient outcomes. Contact centre communications are in scope.

In practice, consumer understanding compliance means plain language scripting, clear disclosure of fees, risks and rights, confirmation that the customer understood before the call ends, and evidence that you've tested and monitored this at scale. For debt collection, customers must also be clearly informed of their rights and what happens if they can't pay.

Consumer support

Consumer support requires firms to provide a level of service that enables customers to realise the benefits of products, exercise their rights and get help when they need it. Contact centres are both the primary delivery mechanism for this outcome and the primary risk point.

The FCA's cross-cutting review on customer journeys is examining friction: are customers facing unnecessary barriers to getting help, making complaints or exercising their rights? Long wait times, excessive IVR routing and agents who can't resolve issues without escalation are exactly the friction points the review is looking for.

For vulnerable customers, the requirements are higher. Firms that cannot demonstrate differentiated consideration for vulnerable customers are not meeting the Consumer Duty standard. For collections contact centres this is particularly acute; contact strategies that take no account of financial vulnerability or hardship indicators are a direct Consumer Duty risk.

Call recording and monitoring: your Consumer Duty evidence layer

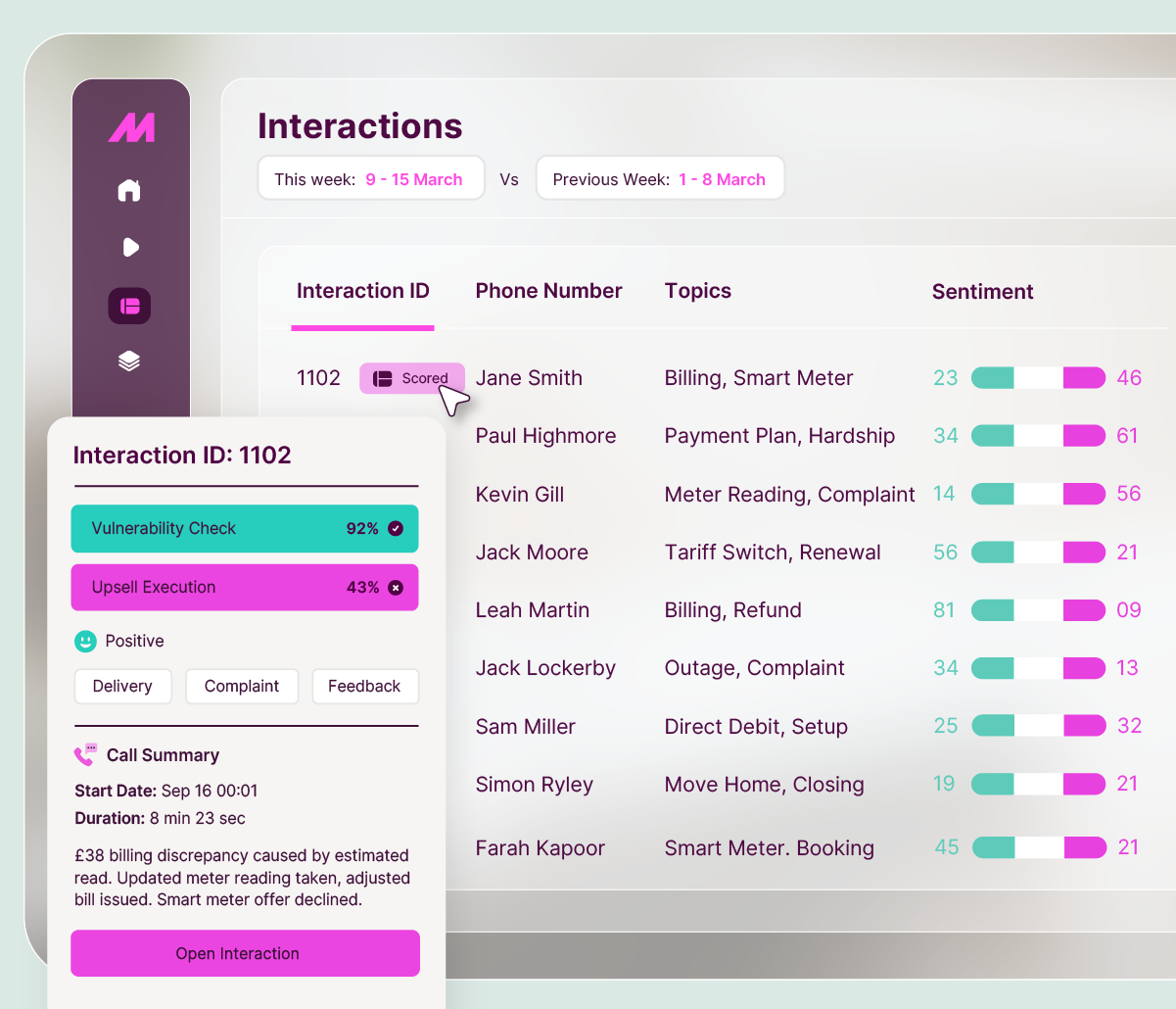

Here's the practical problem Consumer Duty creates for contact centres: you need to demonstrate good outcomes across thousands of calls. You can't do that manually. Call recording and quality monitoring aren't just operational tools. Under Consumer Duty, they're your compliance infrastructure.

The FCA expects firms to have documented, data-driven evidence that their contact strategies are delivering the four outcomes.

In practice, that means call recordings that can be retrieved and reviewed to demonstrate agent conduct and customer treatment; systematic QA scoring against Consumer Duty criteria rather than just internal quality targets; sentiment and outcomes analysis that can identify at scale where customers are experiencing poor outcomes or distress; documented processes for identifying vulnerability indicators during calls; and complaint pattern monitoring to surface systemic issues rather than just resolving individual cases.

The FCA found that many board reports stated actions had been taken without evidence they worked. QA scores and call recording logs that sit in a system but aren't systematically analysed aren't sufficient. The evidence needs to be active, current and connected to outcomes.

FCA call recording compliance: what applies to your contact centre

FCA call recording requirements under SYSC 10A apply to MiFID investment firms; those dealing in financial instruments and arranging transactions. If your contact centre operates in that space, SYSC 10A applies in full: all relevant calls must be recorded, retained for a minimum of five years and be producible on request.

For most debt collection, insurance and general financial services contact centres, the obligation is framed differently but no less real. Under Consumer Duty, if you can't produce call recordings and QA data to evidence agent conduct and customer outcomes, you effectively can't comply. The FCA doesn't prescribe the exact mechanism, but it scrutinises the evidence. Firms without systematic call recording and monitoring have no evidence base to draw on. Record all customer-facing calls, retain them for a period appropriate to your regulatory context (five years is the common standard for FCA-regulated activity), and make sure your QA process is reviewing against Consumer Duty outcomes, not just service standards.

For debt collection contact centres, call recording serves an additional purpose. It's evidence that your collections conduct complies with CONC requirements around contact with customers in arrears. CONC 7.9 sets out what's required; treating customers fairly, not using oppressive tactics, and identifying vulnerability. In an FCA investigation, recordings and QA monitoring logs are what you'll be asked to produce first.

How your contact centre needs to adapt

Evidence by design, not retrospect

The most common Consumer Duty failure mode in contact centres is treating compliance as a report-writing exercise. The evidence needs to exist before the report, in call recordings, QA scores, outcome data and complaints analysis. If you're assembling evidence retrospectively to satisfy a board report deadline, you're already behind.

Build evidence generation into your operational processes: QA scoring frameworks that explicitly test Consumer Duty criteria, outcome tracking at campaign and agent level, and regular complaints analysis that looks for patterns rather than just volume.

Scripting and training

Every agent interaction is a Consumer Duty test. Scripts need to be reviewed against the four outcomes, not just for accuracy but for whether they genuinely help the customer understand and make informed decisions. In debt collection, the language of collections calls can easily cross from firm into oppressive if not carefully calibrated.

Training should make Consumer Duty concrete for agents, not abstract. What does "acting in good faith" mean when a customer says they can't pay? What does "avoiding foreseeable harm" mean when a customer shows signs of financial difficulty? Agents need practical answers to those questions.

Vulnerable customer identification at scale

Manual vulnerability identification; relying on agents to spot and flag vulnerability during calls, doesn't scale reliably at contact centre volumes. You need systematic processes: training that embeds vulnerability indicators, scripting that creates space for customers to disclose, and technology that can flag calls for review based on sentiment or interaction patterns.

For collections contact centres, where a significant proportion of customers may be in financial difficulty, this isn't an edge case. It's a core operational requirement.

Complaints as a compliance signal

Consumer Duty requires firms to use complaints data to identify systemic issues. A contact centre that tracks complaint volumes but doesn't analyse patterns is leaving one of its most valuable compliance signals unused. Complaints analysis should feed directly into QA frameworks, scripting reviews and training programmes, and it should appear in your board report as evidence of how your contact centre identifies and responds to consumer harm signals.

Your 31 July 2026 board report

Your next Consumer Duty board report must be reviewed and approved by your governing body by 31 July 2026. For contact centre operations, the report needs to demonstrate how you monitor outcomes across each of the four pillars, what your call monitoring and QA data shows about customer outcomes, how you identify and respond to vulnerable customer indicators, what your complaints data reveals about systemic issues, and what remediation actions have been taken and whether they worked.

If the answer to any of those is "we don't have that data," the remediation starts now, not on 30 July.

MaxContact's Conversation Analytics, Auto QA and call recording capabilities are built to generate the evidence layer Consumer Duty requires, at contact centre scale, with the audit trail regulators expect to see. Consumer Duty doesn't operate in isolation. Download the UK Contact Centre Regulatory Guide 2025–2027 for a complete view of the regulatory landscape - covering PECR, DUAA, Ofcom CLI, the EU AI Act and more - in one practical resource.

If you're working through what Consumer Duty means for your operation, or want to see how MaxContact supports compliance in debt collection, insurance or financial services contact centres, get in touch.

.avif)

.png)